VISLAND MORTGAGES

Are you working with Visland Mortgages, Nanaimo’s top-rated mortgage brokerage?

We’re here to help every step of the way!

About VIsland Mortgages

Vancouver Island Mortgage is now in full swing with a highly skilled Team that has the capacity to grow the business to new heights.

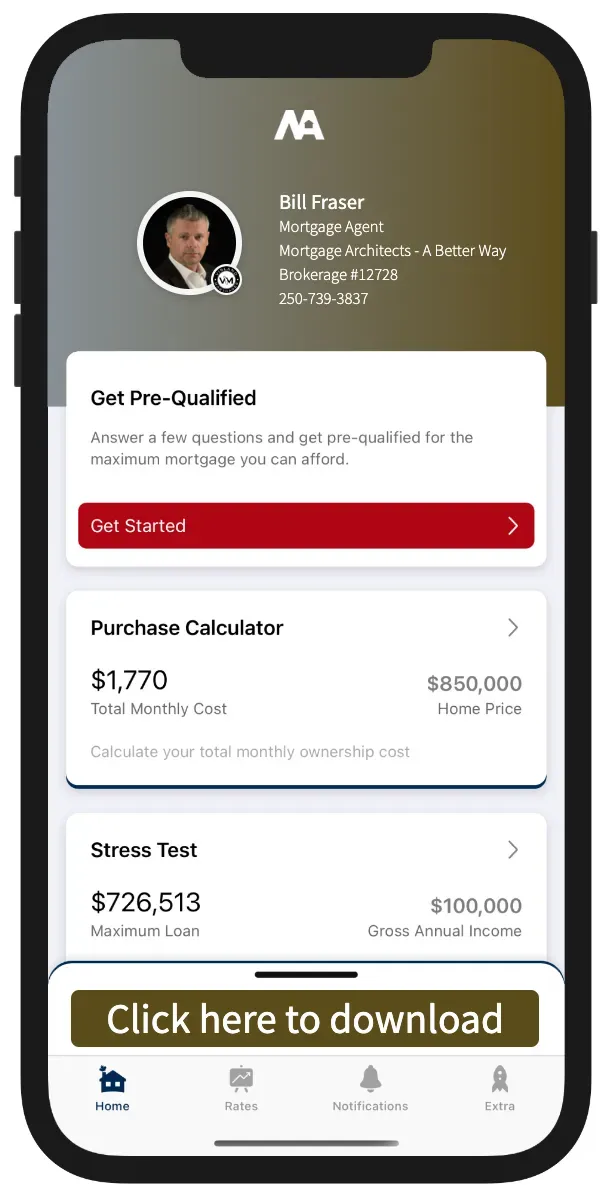

Bill Fraser

Your Personal Mortgage Advisor

Bill has over 20+ years working in the financial industry. Due to his extensive experience and knowledge he works efficiently with all lenders including: banks, credit unions, trust companies, financial institutions and mortgage investment companies.

He is also able to offer his clients a variety of choices within his hundreds of products and services offered. These products include mortgages for purchasing new homes or investment properties, refinancing existing homes, debt consolidation, home equity line of credit, second homes, commercial as well as alternative or private lending.

There is always an option when you deal with Bill Fraser!!

Terrena Huisman

Lending Solutions Specialist - Away on maternity leave

Terrena is the heart and soul of the underwriting team at Visland Mortgages, bringing a sharp eye for detail, a passion for problem-solving, and a genuine commitment to helping clients succeed.

As a Lending Solutions Specialist, trusted realtor lending advisor, and unlicensed underwriting assistant, she works behind the scenes to ensure every file is handled with care, precision, and efficiency. With a strong background as an experienced realtor, Terrena offers valuable industry insight and understands the home buying journey from every angle.

Her intuitive nature, love for numbers, and ability to “put the puzzle pieces together” allow her to find solutions that help make the mortgage process smoother and less stressful for clients and partners alike.

Shanna LaChance

Underwriting Assistant

Shanna is the newest addition to the Visland Mortgages team, bringing a positive attitude, a strong work ethic, and a client-focused approach to every mortgage file she works on. Stepping into the team while Terrena is away on maternity leave, she has quickly become a valued part of our day-to-day operations through her dedication, reliability, and commitment to helping clients have a smooth mortgage experience.

Shanna provides underwriting and administrative support behind the scenes, ensuring every file is organized, accurate, and progressing efficiently from application through to funding. She works closely with the team to keep the mortgage process on track, paying close attention to detail while supporting both clients and lending partners every step of the way.

A 60 second introduction video to

VISLAND Mortgages

Services

Flexible Mortgages

Qualified Advice

No Cost to You

Advocacy

Download My Mortgage Toolbox

Access the calculators in 3 easy steps

WHAT YOU CAN DO WITH MY APP

- Calculate your total cost of owning a home

- Estimate the minimum down payment you need

- Calculate Land transfer taxes and the available rebates

- Calculate the maximum loan you can borrow

- Stress test your mortgage

- Estimate your Closing costs

- Compare your options side by side

- Search for the best mortgage rates

- Email Summary reports (PDF)

- Use my app in English, French, Spanish, Hindi and Chinese

I'M A CERTIFIED REVERSE MORTGAGE SPECIALIST

Let's see if a reverse mortgage is right for you.

LEARN MORE

Lenders

Lenders

I've developed excellent relationships with over 90 lenders across the country. Let's figure out which one has the best product for you.

Bill Fraser & VIsland Mortgages is a proud to partner

and support local organizations

Testimonials

Cindy and Randy Cooper

Shannon and Ashley Hughes

Sam and Nick

Thank You Bill.

Jamie and Vaughn

Thanks again.

Shirley McMillan

Bill, just wanted to send you a quick note of appreciation for your dedication to get me into my very first home! I did not think with my income and the little credit I have, that you would be able to pull this deal off. I have heard you are considered the “Miracle Man” around the island and it sure seems to be true!!!! Lol

Thanks so much, and I am proud to refer you to my family and friends all over BC!!!

Juanita LeMarquand

Mortgage Blog